Could going off the deep end make sense for offshore wind on the US East Coast?

Could the large investor appetite for offshore wind on the American East Coast push the industry ‘off the deep end’ into floating territory?

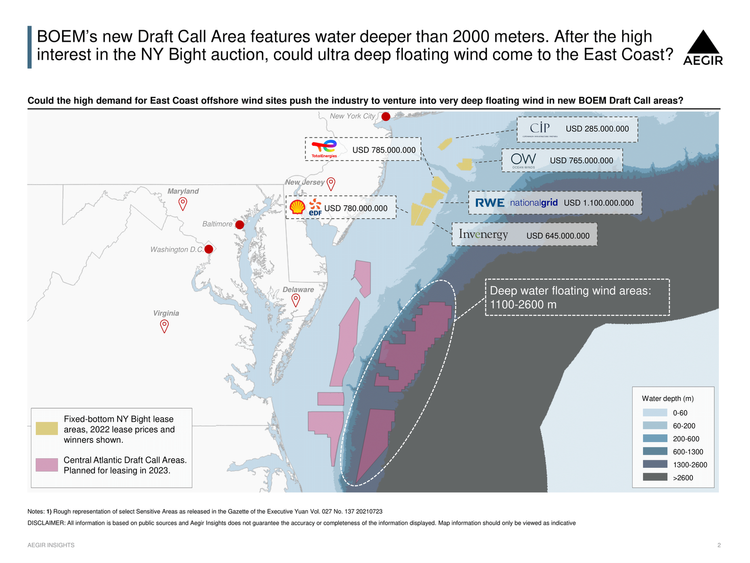

The New York Bight lease auction saw USD 4.37 billion paid in lease fees for fixed-bottom offshore wind areas totalling around 2000 km2 (488,000 acres). As part of Aegir Insights’ Big Float intelligence series on floating wind, we examine the idea of using floating wind off the East Coast to increase available acreage in this coveted region, while avoiding stakeholder issues.

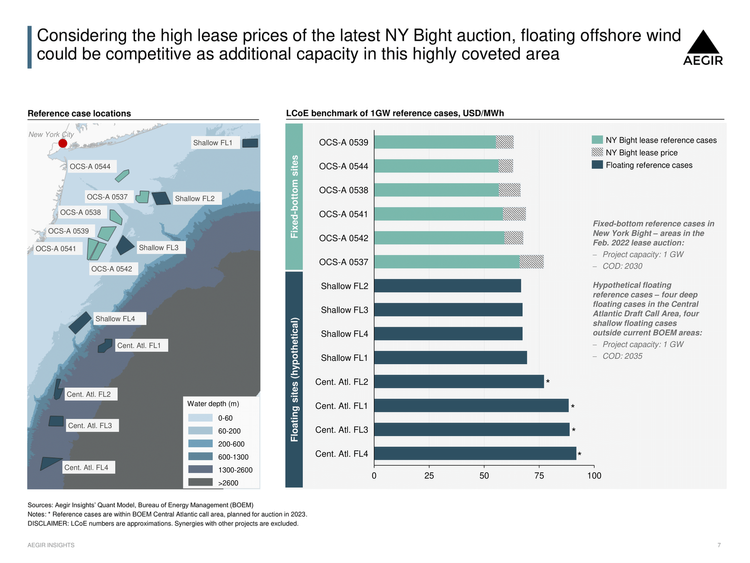

To that end we created a small selection of floating wind reference cases and put them through our Quant model to create a merit order of LCoE of floating wind on the American northeastern coastline.

BOEM already looking to floating on the east coast with deep, Central Atlantic Call Area

With the ambitious offshore wind targets of several states and Biden’s national 30 GW by 2030 target, the Bureau of Ocean Energy Management (BOEM) is picking up the pace of auctions and scouring the sea for the best areas for future offshore wind farms. In 2023, BOEM plans to auction sites in the Central Atlantic Draft Call Area. Six areas are currently under evaluation, the two largest of which are located in waters between 1100 and 2600 meters deep.

Well beyond the depth of any floating wind demonstration projects today and deeper even than BOEM’s West Coast areas, this would be a play for those developers with the most appetite for innovation.

Considering the high demand for acreage, is there a case for very deep floating technology on the US East Coast?

Central Atlantic and New York Bight areas chosen as geographical starting points

Aegir Insights evaluated eight prospective floating offshore wind cases, based in or around areas in which BOEM is already active:

- Four in the New York Bight, but outside existing (fixed-bottom) BOEM areas.

- Four within BOEM’s Central Atlantic Draft Call Area.

In the New York Bight, floating wind could be deployed at depths of 65-80 meters, considered shallow floating and well within the industry’s experience.

The Central Atlantic Draft Call Area, on the other hand, has only deep floating areas. The reference cases here are located in depths up to 2000 meters – yet to be seen in the offshore wind sector, but commonplace in offshore oil and gas.

New York Bight floating wind sites very competitive

Aegir Insights’ LCoE benchmark shows that the most competitive floating sites in the New York Bight area could possibly be utilized at similar costs to the New York Bight fixed leases, when including lease prices in the cost for fixed-bottom wind areas. This indicates that floating might be a competitive option for extending capacity in the region, in particular if the leases for floating wind are cheaper, which would be expected.

Central Atlantic cases sit lower in the merit order due to their exceptionally deep waters bumping up costs for technical solutions. Innovation in floater and mooring concepts may be required to unlock their potential.

Reach out to learn more about Aegir Insights’ subscription-based offshore wind intelligence and Aegir Quant investment solution.