Power Up: Mapping the AC/DC fabricators of offshore substations

Offshore substations are usually framed as a fabrication-yard story. But the real bottleneck sits in OEM relationships.

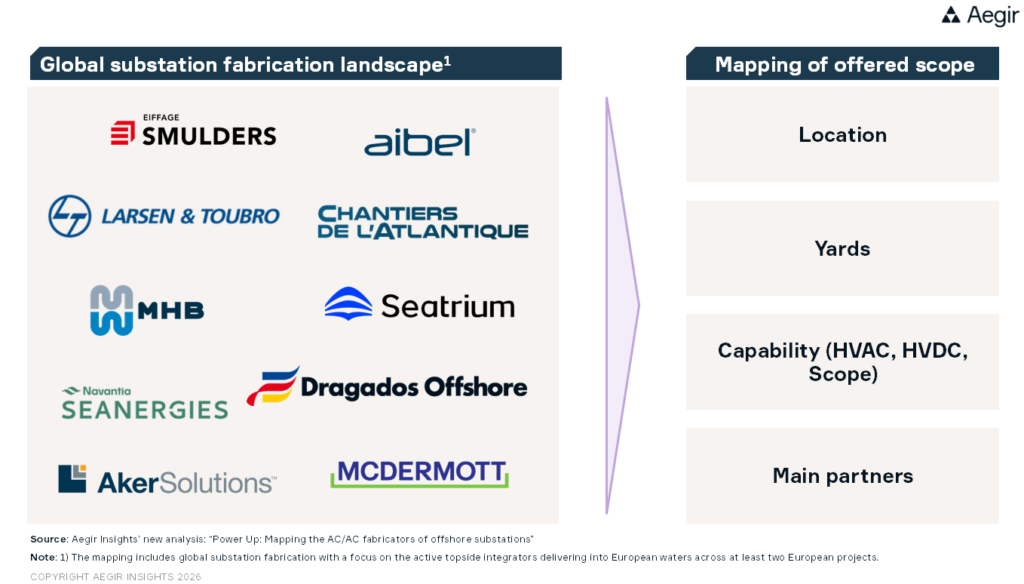

Growing offshore wind ambitions and the shift to more HVDC transmission are driving demand for offshore substations. But the fabrication capability remains concentrated among a small pool of qualified suppliers.

Aegir Insights has mapped the AC/DC fabricators delivering offshore substations into European waters. Our analysis (available to clients here) points to one structural finding: While the HVAC scope stays price-led, the HVDC offshore substation market doesn't compete on yards. It competes on OEM partnerships.

- Three OEMs — GE Vernova, Hitachi Energy and Siemens Energy — have held HVDC converter technology since the segment opened in 2010.

- HVAC scopes stay price-led and competitive; HVDC scopes are multi-year commitments to OEM-fabricator consortia.

- Almost half of the yards delivering into European waters now sit in Asia or the Gulf.

What does this mean for developers, TSOs and equipment suppliers planning the next decade of OSS scope?

Offshore substations lead times and order books

Offshore substations (OSS) are the single most schedule-critical procurement decision in offshore wind. Yet, commissioning timelines vary significantly depending on transmission type and who is procuring the platform.

Aegir Insights' OSS Order Book tracks this dynamic across 150+ orders globally – a stark difference that emerges from the data is the lead time difference in TSO-lead vs. developer-lead OSS contracts.

Learn more about our available data on OSS.

Aegir Newsletter: Stay up-to-date with development in renewable energy and new analysis by Aegir Insights

Delivered straight to your inbox, Aegir Insights' intelligence newsletter will sharpen your market insight with exclusive analysis on key markets, developments, and technologies shaping onshore wind, offshore wind and storage/hybrids.