With visions of having 15GW-plus of deepwater arrays in place by the end of the decade now on a receding horizon, could a two-wave industrialization strategy carry the sector into commercialization by 2035, asks Victoria Toft

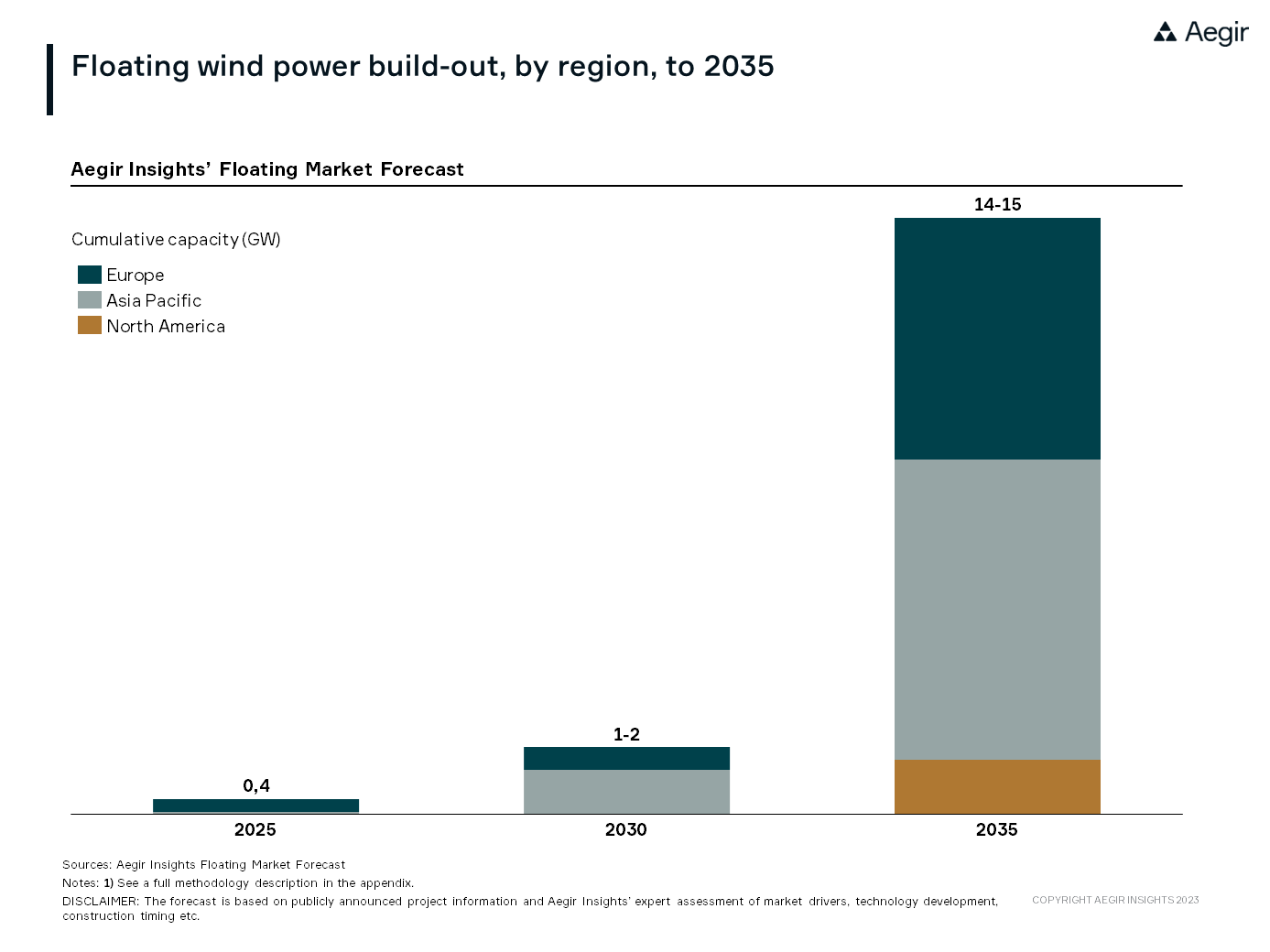

Floating wind may be far off track reaching earlier prognostications that as much as 16.5GW would be turning by the end of the decade, but Aegir Insights sees a two-wave development cresting through to 2035 that could bring a first 14GW of deepwater plant online – and more importantly establish the sector’s industrialization and key role in the global offshore wind built-out now gathering pace.

Expanding the current 250MW fleet to such a international industrial armada – the total pipeline of announced floating projects today stands near 400GW – remains an unprecedentedly challenging feat, needing not just the core technologies offshore, but also the new coastal construction infrastructure that will have to be ready for the hatchling sector, whose progress requires a measured and strategic outlook on capacities and especially future cost developments.

Aegir’s ‘central’ forecast is that 1-2GW of floating wind could be operational by 2030, before the sector streamlines and installs as much as another 12GW in the five years to follow. ‘Early innovators’ will carry ‘first MW’ premium for their projects, benefiting in the long run, but paying over the odds in the near-term, in higher-cost less-mature technology and small-scale deployment.

The big industrialization updraft will come with the second wave: New entrants and ‘fast followers’ that can capitalize on the sector’s early learnings and new-built construction infrastructure.

'The big industrialization updraft will come with the "second wave" and capitalization on the floating wind’s early learnings and new-built construction infrastructure'

Victoria Toft

Head of Data

Aegir Insights

As floating wind’s costs tumble toward parity with bottom-fixed, other regions will seize the opportunity to get onboard, creating the conditions in a number of markets to make the leap directly to 100-300MW ‘stepping stone’ or even commercial-scale projects rather than build pilots. These countries will have the added advantage of using the early innovators’ learnings to speed the cost-out.

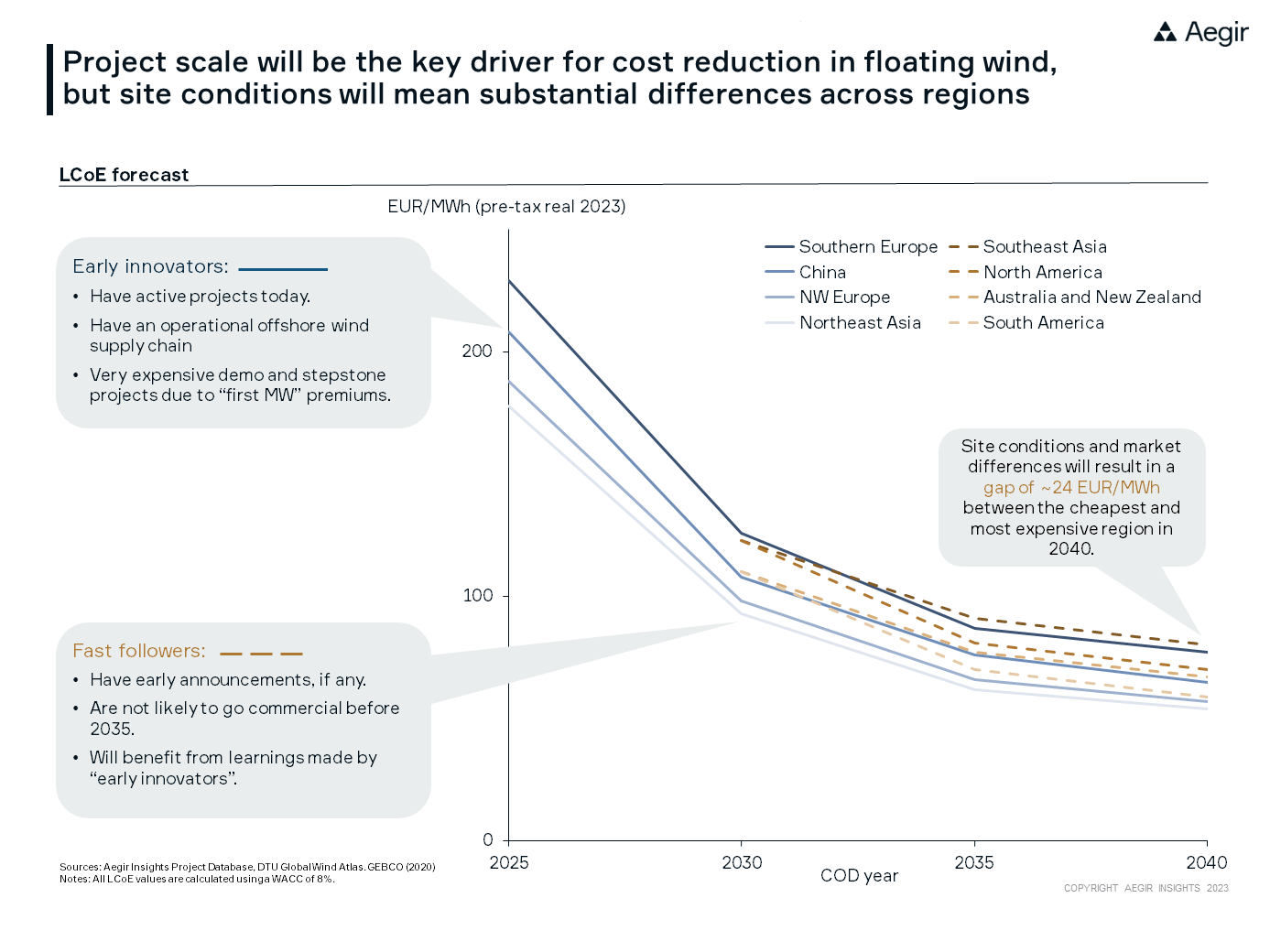

Levelized cost of energy is expected to progressively decrease in the coming years, with prices projected to decline towards €70/MWh ($75/MWh) by the end of the 2030s, accelerated by the post-2035 build-out, though this development would happen at different paces in different regions.

However downcast moods may be in the sector, 2023 was in fact a banner year, with the largest-ever floating wind array, the 95MW Hywind Tampen, brought into production off Norway, French flagship project, the 25MW Provence Grand Large, in commissioning, and the first 100MW stage of Power China’s Southeast Wanning project kicking off preparation off China’s Hainan province.

Meanwhile, though postponed, Norway appears destined to hold a first floating auction in 2024, while in the UK, the Crown Estate has enlarged its first deepwater tender by 500MW to 4.5GW. In Asia-Pacific, Australia’s unveiled offshore wind ‘mega zones’ include two in water depths too deep for bottom-fixed, and in Japan, offshore wind development areas have been updated to encompass two new sites for floating pilots.

Floating wind’s commercial take-off may well be postponed by the general uncertainties in the offshore wind market today and lack of route to market, but if the 'early innovators' get it right and 'fast followers' run with it, Aegir's high-case scenario for the sector has 5GW spinning by 2030 and over 25GW five years later.

Interested in getting the latest insights on developments in the global floating wind market? Aegir Insights has just released the Floating Wind Intelligence package for Q3 2023 to subscribers, including the tracking of projects, partnerships and high-quality market forecasts based on our extensive industry experience in market and project development. Reach out to us to learn more about Aegir Insights' floating intelligence.

This article was first published in Aegir Insights' intelligence newsletter, Beaufort.

Delivered straight to your inbox every Sunday, Beaufort will sharpen your market insight for the week ahead with exclusive commentary, analysis, and in-depth journalism delving into the talking points and technologies shaping offshore wind.