Aegir Insights this week released its quarterly floating intelligence package to clients, including updates on country forecasts, projects and partnerships in this fast-changing space. Ambitious floating projects and intentions continue to be announced across the world, but where is the pre-2030 capacity ‘really’ emerging?

CHINA MAY BE THE FIRST MARKET TO REACH GW SCALE FLOATING WIND

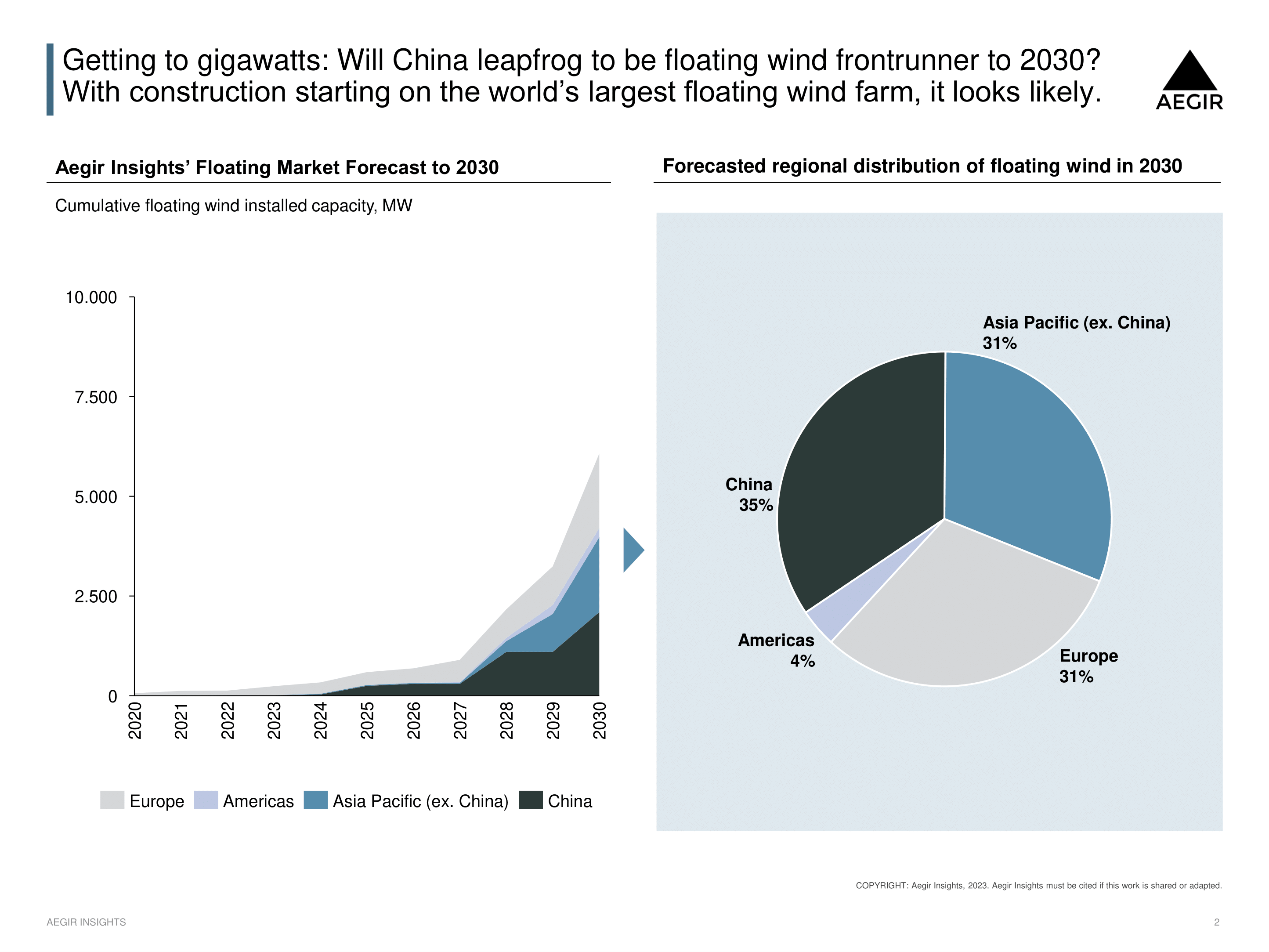

All indications are that China could leapfrog to be the first country to reach GW scale, despite having been a late starter compared to Europe. PowerChina has just broken ground on the first phase (200 MW), expected to take claim as the world’s largest floating project, and then continue to be the first GW scale in a later extension. But, Aegir Insights’ quarterly update also shows a bright future in other regions.

US, TAIWAN, NORWAY AND THE UK MOVE AHEAD ON FLOATING WIND

United States: California completed the first deep floating lease auction in December 2022. Developer announced capacities across the sites amount to 8.6 GW which could be coming online by mid 2030s

Taiwan: New details have been announced about a planned tender, with expectations for an auction in Q4 of 2023 for two projects

Norway: The highly anticipate 2023 auction competition is heating up, set to include 3 x 500 MW of floating wind

United Kingdom: The application window for INTOG projects closed in November 2022 and results are expected by the end of April 2023

2022: A YEAR OF EVER-EXPANDING FLOATING WIND HORIZONS

2022 was very much a year of expanding market horizons. In 2023, supply chain and route-to-market will have growing focus, should GW scale happen before 2030.

Aegir’s clients can reach out to schedule a bespoke walk through of these floating insights.